This Article explain everything about Blockchain Technology, From Origin of Blockchain Technology, Core Features of Blockchain Technology, Advantages or Importance of Blockchain Technology, to All Types of Blockchain Technology We find Out, Base on Our Research.

We Hope This Article Will Be Helpful to Our Daily Users, and 360Hausa Team Will Be Updating This Article To reflect with time.

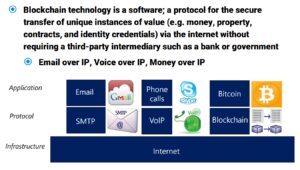

What is Blockchain Technology?

The concept of Blockchain Technology came into existence from the first cryptocurrency, Bitcoin. It is a very new, complex and trusted technology, and researchers are working continuously to find a way to apply this disruptive technology in different areas. Blockchain is a very disruptive technology that can reconfigure all aspects of society and its operations. This technology is immutable and distributed, making it difficult for transactions to be changed, duplicated, or faked.

A blockchain is essentially a distributed database of records or public ledger of all transactions or digital events that have been executed and shared among participating parties. Each transaction in the public ledger is verified by consensus of a majority of the participants in the system. And, once entered, information can never be erased. The blockchain contains a certain and verifiable record of every single transaction ever made. To use a basic analogy, it is easy to steal a cookie from a cookie jar, kept in a secluded place than stealing the cookie from a cookie jar kept in a market place, being observed by thousands of people.

Bitcoin is the most popular example that is intrinsically tied to blockchain technology. It is also the most controversial one since it helps to enable a multibillion-dollar global market of anonymous transactions without any governmental control. Hence it has to deal with a number of regulatory issues involving national governments and financial institutions. However, Blockchain technology itself is non-controversial and has worked flawlessly over the years and is being successfully applied to both financial and non-financial world applications.

Last year, Marc Andreessen, the doyen of Silicon Valley’s capitalists, listed the blockchain distributed consensus model as the most important invention since the Internet itself. Johann Palychata from BNP Paribas wrote in the Quintessence magazine that bitcoin’s blockchain, the software that allows the digital currency to function should be considered as an invention like the steam or combustion engine that has the potential to transform the world of finance and beyond. Current digital economy is based on the reliance on a certain trusted authority.

Our all online transactions rely on trusting someone to tell us the truth—it can be an email service provider telling us that our email has been delivered; it can be a certification authority telling us that a certain digital certificate is trustworthy; or it can be a social network such as Facebook telling us that our posts regarding our life events have been shared only with our friends or it can be a bank telling us that our money has been delivered reliably to our dear ones in a remote country.

The fact is that we live our life precariously in the digital world by relying on a third entity for the security and privacy of our digital assets. The fact remains that these third party sources can be hacked, manipulated or compromised. This is where the blockchain technology comes handy.

It has the potential to revolutionize the digital world by enabling a distributed consensus where each and every online transaction, past and present, involving digital assets can be verified at any time in the future. It does this without compromising the privacy of the digital assets and parties involved. The distributed consensus and anonymity are two important characteristics of blockchain technology.

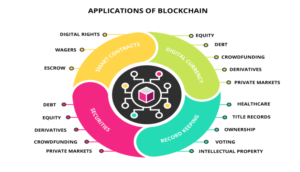

The advantages of Blockchain technology outweigh the regulatory issues and technical challenges. One key emerging use case of blockchain technology involves “smart contracts”. Smart contracts are basically computer programs that can automatically execute the terms of a contract.

When a pre-configured condition in a smart contract among participating entities is met then the parties involved in a contractual agreement can be automatically made payments as per the contract in a transparent manner. Smart Property is another related concept which is regarding controlling the ownership of a property or asset via blockchain using Smart Contracts. The property can be physical such as car, house, smartphone etc. or it can be non-physical such as shares of a company.

It should be noted here that even Bitcoin is not really a currency–Bitcoin is all about controlling the ownership of money. Blockchain technology is finding applications in wide range of areas—both financial and non-financial. Financial institutions and banks no longer see blockchain technology as threat to traditional business models. The world’s biggest banks are in fact looking for opportunities in this area by doing research on innovative blockchain applications.

In a recent interview Rain Lohmus of Estonia’s LHV bank told that they found Blockchain to be the most tested and secure for some banking and finance related applications. Non-Financial applications opportunities are also endless. We can envision putting proof of existence of all legal documents, health records, and loyalty payments in the music industry, notary, private securities and marriage licenses in the blockchain. By storing the fingerprint of the digital asset instead of storing the digital asset itself, the anonymity or privacy objective can be achieved.

In this report, we focus on the disruption that every industry in today’s digital economy is facing today due to the emergence of blockchain technology.

Blockchain technology has potential to become the new engine of growth in digital economy where we are increasingly using Internet to conduct digital commerce and share our personal data and life events. There are tremendous opportunities in this space and the revolution in this space has just begun. In this report we focus on few key applications of Blockchain technology in the area of Notary, Insurance, private securities and few other interesting non-financial applications. We begin by first describing some history and the technology itself.

Most simply, the blockchain is defined as the decentralized and distributed ledger technology that provides information to be recorded, maintained and shared by a community. It is a new type of database having digital records of transactions. No person or entity has control over it, and none of them can go back and erase or change a transaction history. Distributed ledger technology combines transparency, immutability and security for the participants of the network. It is nearly impossible to hack or attack the entire system based on blockchain technology because of the distributed nature of this technology.

Thus, blockchain is a tamperproof technology. In blockchain technology, all transactions performed in the past cannot be changed or deleted. So, it provides transparency and immutability to all transactions that happened in the past (Kushwaha & Singh, 2020). “Unlike the Web or Internet alone, blockchains are distributed, not centralized; open, not hidden; inclusive, not exclusive; immutable, not alterable; and secure. Blockchain gives us unprecedented capabilities to create and trade value in society” (Tapscott & Tapscott, 2017).

Like any other technology revolution, the blockchain technology revolution may also be categorized into three phases as Blockchain 1.0, Blockchain 2.0 and Blockchain 3.0 (Kushwaha & Singh, 2020). Cryptocurrencies are an application of Blockchain 1.0, which is related to dayto-day digital payment-based systems. Blockchain 2.0 is associated with the whole economic market, where Blockchain technology is used to expand traditional transactions like bonds, stocks, shares and smart contracts. While all those applications which are not included in the scope of Blockchain 1.0 and 2.0 come under Blockchain 3.0, like e-governance, digital health records, digitally vote counting, science, literacy, culture and digital art (Swan, 2015).

However, the applications or usage of blockchain technology are now being explored in many other areas. Currently, industry sectors such as finance, medicine, health science, education and government are making significant investments, investigating the transformational impact of blockchain and searching the future opportunities of implementing this technology in many other sectors, Blockchain has been found as an excellent solution for many issues encountered by the educational community.

It can be used for multiple works like issuing, monitoring, validating and sharing the certificates (Kolvenbach, Ruland, & Grather, 2018). Hoy (2017) suggested that blockchain can also be used as another digital rights management tool. This technology has potential use not only in the financial domain but also in the non-financial domains. Thus, it can be used as a catalyst in developing the library & library services to accelerate the entire library system globally.

Origin of Blockchain

Short comings of current transaction system: » Cash is useful only in local transactions and in relatively small amounts. » The time between transaction and settlement can be long. » Duplication of effort and the need for third-party validation and/or the presence of intermediaries add to the inefficiencies. » Fraud, cyberattacks, and even simple mistakes add to the cost and complexity of doing business, and they expose all participants in the network to risk if a central system, such as a bank, is compromised. » Many people in the world don’t have access to a bank account and have had to develop parallel payment systems to conduct transactions. And transaction volumes will explode with the rise of Internet of Things (IoT)

What is Blockchain?

The name of blockchain came from its structure, i.e. block and chain; individual records, called blocks, are linked together in a series to form the chain. Blockchain is an emerging technology that will change the way we acquire and share information. It is an online global database that anyone, anywhere at any time, with an internet connection, can use. Like traditional databases, it is not owned by any central agency or body like banks and governments. Thus, Hacking or tampering with the entire system based on this technology by faking transactions, documents, and any information becomes nearly impossible.

All financial transactions based on this technology are more fast and secure than the traditional ones. Blockchain technology combines many other technologies, like cryptography, peer-to-peer networks, smart contracts, and consensus mechanisms to create a new and unique database. It also logs the time, date, details of participants, and other legal or contractual portions of every transaction.

Blockchain is the primary technology behind cryptocurrencies like Bitcoin and Ethereum, making it secure for trading digitally by verifying and storing transaction records in a distributed and time stamp manner. The term Bitcoin, a cryptocurrency, was first introduced in 2008 by Satoshi Nakamoto in his work named “Bitcoin: A Peer-to-Peer Electronic Cash System” (Hoy, 2017).

How does Blockchain Works?

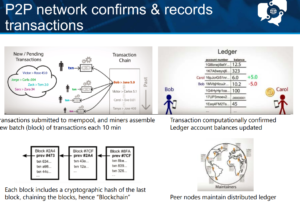

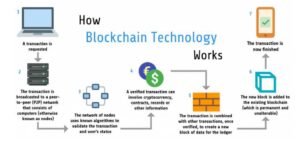

In general, Blockchain is a chain of blocks, and a block consists of three things: Data, Hash, and Hash of the previous block. Each block in the chain contains a cryptographic hash of its own and the last block to stay connected in the chain. A Block is a primary unit of blockchain. In the blockchain, a block is a collection of data or information. The information is added to the block in the blockchain by connecting it with other blocks in chronological order and creating a chain of blocks linked together.

Thus, it forms a chronological database of transactions that is shared with multiple nodes, i.e. computers or servers, in a network. The unique number added to a hashed or encrypted block called Nonce that can be used only once is selected by the miners to solve a cryptographic puzzle for generating the next block in the chain. It is known as Proof of Work. A Hash is a unique alphanumeric identifying code or number generated when any transaction happens in the blockchain. Hash is based on data of its own, a hash of the previous one, and its timestamp (Peck, 2017).

When a transaction happens in the blockchain, that transaction is recorded in a block, and that block must be validated before adding it into the chain. The authenticity of a block 5 | P a g e must be verified through a consensus algorithm in which the majority of nodes (clients or servers) and the nodes having the highest stack in the chain of the distributed network must validate the block before adding to it in a chain. After the validation of the block, a unique, identifying code, i.e. a hash, is generated.

By doing this, we do not need any third-party interference to validate or to do transactions. Blocks can be recognized by their block number or block height and block header hash. The data in the blocks is detected through a computerized algorithm known as the hash function. This function locks the data to be seen by the participants in the Blockchain and makes the data immutable. Every block has its own hash function. In Blockchain, the data is recorded for permanent and will not be changed. A small change in it generates a new block in the chain. Blockchain works like a digital notary with time-stamps to avoid tampering with any information.

Core Features of Blockchain Technology

- In the blockchain, Blocks can be written and read by certain and authentic participants, and all entries are permanent, transparent, and searchable.

- All transactions in blockchain technology are recorded in chronological order on a continuously growing and permanent database.

- Blockchain is a tamper-proof technology. It is nearly impossible to hack or attack the entire system based on blockchain technology because of its distributed nature.

- In this technology, data is replicated and stored across the system over a peer-to-peer network.

- It facilitates the peer-to-peer transfer of value without a central intermediary like- a bank or any financial institution.

- In the blockchain, digital signatures and cryptography are used to secure the transaction.

- In blockchain technology tokenization process is followed where the value of an asset (physical or digital) is converted into digital tokens that are recorded and shared via blockchain.

- It is significantly faster & cost-efficient technology than conventional methods by eliminating intermediaries and replacing remaining manual processes.

Some Key Advantages of Blockchain Technology

▪ Real-Time Transaction Settlement

▪ More Security & Transparency

▪ No Third-Party Involvement

▪ Durability & Reliability

▪ Immutability

▪ Cost Saving

▪ User Pseudonymity

Types of Blockchain Technology

Blockchain technology is primarily of two types; Public blockchain and Private blockchain, but two other forms of blockchain also exists; Hybrid blockchain and Consortium or Federated blockchain. The brief discussion on all types of blockchain, as mentioned above, are as follow:

Public Blockchain: Public blockchains are such blockchains that are accessible publicly. It is a type of blockchain, “for the people, by the people, and of the people” (Sanjay & Nabi, 2020). A public blockchain is permission-less distributed ledger technology where anyone (node or end-user) may join and do the transactions. They do not require unique authentication (login with user id & password) to access, read, write, and update the blockchain. This technology is used in cryptocurrencies like Bitcoin, Ethereum & Litecoin etc.

Private Blockchain: A private blockchain is permission-able or restrictive blockchain technology, functional only in a closed network. This blockchain is usually used within an organization or firm where only authentic members can access and do the transactions in the network. Participants of this network require unique authentication or authorization (login with user id & password) to access, read, write and update in the blockchain. Such blockchains are generally less-trusted than public blockchains. A private blockchain can be used in voting, digital identity & supply chain management etc.

Hybrid Blockchain: A Hybrid blockchain is a combination of both Public and Private blockchains. Such blockchain uses the features of both types of blockchain. “A transaction in a private network of a hybrid blockchain is usually verified within the same network, but participants may also release it in the public blockchain to get verified.” The organization that neither wants to deploy a private blockchain nor public blockchain can simply deploy this blockchain. Example: Dragonchain.

Consortium Blockchain: Consortium blockchain is also known as Federated blockchain. This blockchain network is managed by a set of organizations or nodes rather than a centralized or decentralized network. It is an ideal solution that requires collaboration across the board. For instance, supply chain, food, and medicine would need an alliance across brands. Example: Energy Web Foundation, Ripple etc.

Conclusion

Blockchain is a public ledger where transactions are nearly impossible to amend. A decentralized database where business is transparent without any involvement of the middleman. The first use of blockchain technology was the digital currency (bitcoin). However, other potential uses of this technology are yet to be explored. It is expected to have an impact on cyber security, internet of things, supply chain management, market prediction, governance, information management, financial transactions and more application domains. Till today, blockchain has redesigned the way people deal with their money due to its effectiveness, especially in terms of security.

Blockchain is shorthand for a suite of distributed ledger technologies that can be programmed to record and track anything of value, such as financial transactions, medical records, land titles, and so on. Blockchain technology is based on the centuries-old method of the general financial ledger. In simplified language, it is a digital ledger which holds the records of all sorts of transactions that happen in a peer-to-peer network. This technology is assumed to ‘cut out the middleman’ from any sort of transaction or transfer of digital assets. This is a much more secure and decentralized medium. Financial institutions are exploring the possibilities of using this technology to ensure secure transactions.

The history of blockchain is not that old. The first step of blockchain was initiated in 1991 by Stuart Haber and W. Scott Stornetta, with their work on a cryptographically-secured chain of blocks, where no one could tamper with the time stamps of documents. In 1992, they upgraded their system to incorporate Merkle trees, to allow the system to accept more documents in a single block. However, the blockchain that we know today was introduced by Satoshi Nakamoto in 2008. He is known as the brain behind blockchain technology. Many people believe that he could be the person, or one of a group of people, who worked on bitcoin for the first publicly-known application of digital ledger technology (DLT). Satoshi released a white paper on blockchain, explaining all the details of the technology in 2009, and from there, the development of blockchain has gone far, with many implementations.

{kind=link}